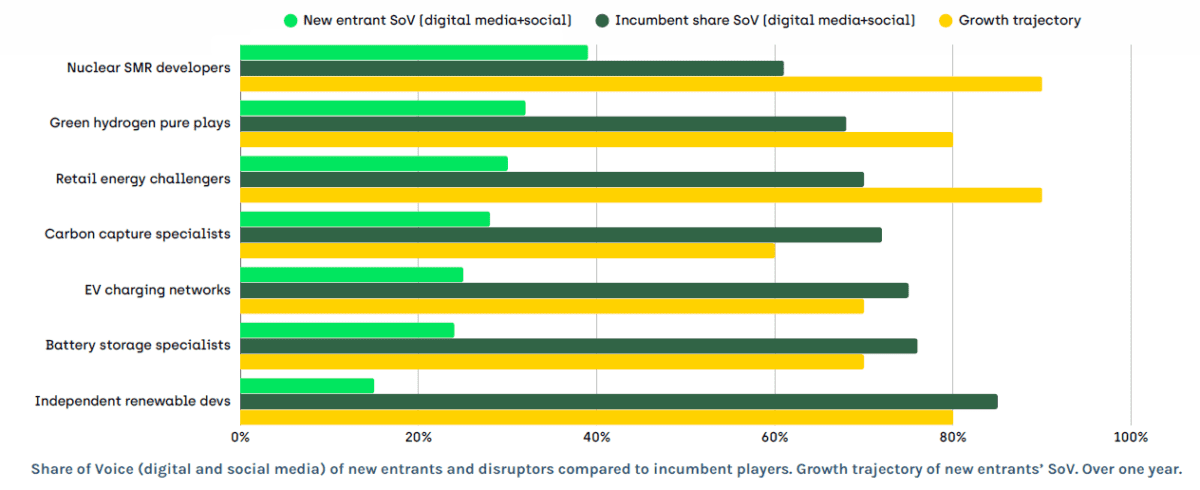

Onclusive tracked 16.6 million mentions across 86 energy companies over twelve months. The data reveals a pattern that competitive intelligence professionals will recognise, and that communications directors should find urgent: energy sector disruptors. New entrants now account for 39% of all nuclear SMR media conversation, 32% of green hydrogen coverage, and 30% of retail energy challenger narratives. Growth trajectories in all three categories score 8 or 9 out of 10 – meaning these positions are still rising.

This blog explains exactly how Octopus Energy, Stegra, and NuScale built those positions, why size and resources are insufficient to dislodge them, and what the practical signals are for identifying your own disruptors before they reach the same point of consolidation.

Energy sector disruptors: The narrative has already shifted

There is a concept in competitive strategy called first-mover advantage. In media and communications, the equivalent is narrative ownership: the ability of one player to define the terms of a conversation before competitors have the chance to respond. In the energy sector, a group of challengers have achieved exactly that – not in the markets they entered, but in the stories being told about those markets.

Onclusive’s Energy Industry Scan 2026 identifies a structural shift in how the energy conversation is being won and lost. In three specific categories – nuclear SMR development, green hydrogen production, and retail energy – energy sector disruptors have captured narrative shares that major incumbents, for all their resources and reach, are struggling to match.

The numbers are unambiguous: New entrants now account for 39% of all nuclear SMR media conversation, 32% of green hydrogen coverage, and 30% of retail energy challenger narratives. In each case, the growth trajectory is rated at 8 or 9 out of 10, meaning the share is not static – it is still rising.

For communications directors, competitive intelligence professionals, and PR strategists working in or around the energy sector, these figures are not just interesting data points. They are an early warning system. The window for incumbents to respond is narrowing with each reporting cycle, and understanding why requires a close look at how these challengers built their positions – and what makes those positions so difficult to dislodge.

Three disruptors, three playbooks

Octopus Energy: consumer engagement as a durable asset

Of all the energy sector disruptors tracked in Onclusive’s dataset, Octopus Energy’s second-place ranking in new entrant share of voice – at 23.6% across social and digital media – is the most strategically meaningful signal.

Unlike the category’s clear outlier, Tesla Supercharger (which holds 40.7% on the strength of Elon Musk’s personal media gravity and the broader Tesla brand ecosystem), Octopus Energy’s share of voice is structurally different in origin. It is not inflated by a celebrity founder effect (Elon Musk), a parent brand, or a viral moment. It has been built, methodically, through sustained consumer engagement on substance: tariff innovation, heat pump rollout, smart metering, international expansion across 18 countries, and a consistent record of generating positive earned media in a sector where most incumbents attract coverage primarily through price increases, regulatory disputes, or service failures.

That distinction matters enormously for competitive intelligence purposes. Celebrity-driven or event-driven SOV is fragile – it rises and falls with the individual or the story. Octopus Energy’s media position reflects something harder to acquire and harder to disrupt: a reputation for doing what it says it will do, at scale, in a market that has given consumers ample reason for scepticism.

The implication for legacy utilities is pointed. Competing with Octopus Energy on tariff communications or sustainability messaging is not simply a matter of producing more content or spending more on media. The earned credibility that Octopus has accumulated – the kind that comes from third-party commentary, consumer advocacy, and consistent analyst coverage – cannot be purchased. It has to be earned, and that takes time that incumbents may not have.

Stegra: the power of a single, clear narrative

Stegra’s visibility in the green hydrogen and industrial decarbonisation space is, on the surface, paradoxical. Its social media volume is modest. It does not have the consumer brand recognition of Octopus or the cross-sector reach of Tesla. Yet within the channels that matter for its audience – the financial press, specialist industry media, and climate policy reporting – it consistently occupies a prominent position disproportionate to its size.

The explanation lies in what Stegra represents: the world’s first steel mill to use green hydrogen on a large scale, under construction in Boden, Sweden. That single, concrete, specific claim sits at the intersection of three of the dominant media narratives for 2026: industrial decarbonisation, European energy sovereignty, and the credibility of green hydrogen as a commercially viable technology. It is not abstract or a pledge or a roadmap but a named facility, in a named location, doing a named thing – and that specificity is exactly what specialist and institutional media reward.

For energy communicators, Stegra’s case reveals a principle that applies far beyond green hydrogen. Narrative ownership in specialist media does not require volume. It requires clarity. A single, well-defined story that addresses a concrete question – “can green hydrogen actually work at industrial scale?” – generates more durable coverage than a hundred press releases about ambition and commitment. Stegra does not have to explain what it is doing or why it matters. The story explains itself.

That is a competitive position no incumbent can replicate simply by announcing a similar project. The first-mover premium in narrative terms accrues to the company that defines the category, not the company that joins it.

NuScale and X-energy: winning the conversation before the product exists

Perhaps the most interesting finding in the Onclusive data is the performance of nuclear SMR developers. NuScale Power holds 3.6% of new entrant share of voice and X-energy holds 3.0% – together with Rolls-Royce SMR (2.4%), they contribute to a new entrant share of 39% in a category that did not meaningfully exist as a media narrative five years ago.

What makes this particularly notable is that none of these companies yet operates a commercial SMR facility. The conversation is being won on the basis of roadmaps, regulatory submissions, partnership announcements, and the narrative positioning of SMR as the answer to the hyperscaler electricity demand problem – the challenge of powering AI data centres with reliable, low-carbon baseload power.

The media logic here is important for competitive intelligence professionals to understand. In an environment where the AI electricity demand shock has become one of the defining energy stories of 2026, SMR developers are positioned as the solution to a problem that is real, urgent, and not yet solved. That positioning generates coverage not because the product is operational, but because the narrative addresses a live anxiety in the market.

Incumbents who have invested in nuclear for decades are not achieving equivalent narrative share in this category, not because their technology is inferior, but because they did not define the category on terms that connect directly to the AI demand story. The SMR developers did. And the media window they opened is significantly harder to enter once the challenger has established the frame.

Why incumbents can’t simply reclaim this ground

Understanding why energy sector disruptors retain narrative advantage requires understanding what creates narrative ownership in the first place – and why size and resources are insufficient to reclaim it.

Credibility cannot be manufactured

The earned media that drives Octopus Energy’s SOV is generated by third parties: journalists, analysts, consumers, and industry commentators who have chosen to write about the company on the basis of what it has done. When a legacy utility attempts to reposition itself as a customer-centric challenger, the gap between its stated positioning and its track record creates a credibility problem that communications investment alone cannot close.

Narrative first-movers set the terms of evaluation

Stegra defined green hydrogen steel on its own terms. Any incumbent entering the same space will be evaluated against Stegra’s benchmark, not against its own. The question journalists will ask is not “what is this company doing?” but “how does this compare to what Stegra is already doing?” The first-mover sets the standard; the follower responds to it.

Growth trajectories compound

Onclusive’s data assigns growth trajectory scores of 8-9 out of 10 to the three categories where new entrants are leading. These are not stable positions – they are rising. The narrative share challengers hold today will be larger in the next reporting cycle, and the next. The window for incumbents to invest credibly in competitive positioning narrows with each iteration.

Scale creates vulnerability, not advantage

Large incumbents operating across multiple categories simultaneously face a structural disadvantage in narrative terms: their communications resources are distributed across a broader set of narratives, while challengers can focus everything on a single story. Octopus Energy communicates almost exclusively about retail innovation. Stegra communicates almost exclusively about the Boden mill. NuScale communicates almost exclusively about SMR as the solution to the baseload problem. That focus generates intensity of coverage that diversified incumbents cannot match in individual categories.

The four categories incumbents still control – and why that may not last

The Onclusive analysis identifies four categories where incumbents retain dominant narrative control: EV charging, battery storage, independent renewable development, and carbon capture. In each case, however, the data contains warning signals that communications teams should not ignore.

EV charging is dominated by Tesla Supercharger, which holds 40.7% of new entrant SOV in the category. Remove that single outlier – which is better understood as a consumer technology narrative than a pure energy narrative – and pure-play charging networks are marginal. The apparent incumbent strength in this category is partly an artefact of Tesla’s classification. Pure-play EV charging challengers like Ionity and Pod Point operate in an entirely different visibility register. The category is more contested than aggregate figures suggest.

Battery storage specialists and independent renewable developers remain narratively marginal despite strong operational roles in the energy system. Their coverage is absorbed by the utilities and oil majors that commission the assets they enable – a pattern that reflects a genuine communications vulnerability. As these companies grow and seek their own capital market relationships, the incentive to build independent narrative presence increases. The transition from invisible supplier to visible player can happen quickly when a company has operational milestones to announce.

Carbon capture holds a moderate challenger share but the lowest growth trajectory of the seven categories analysed, at 6 out of 10. The combination of technical complexity, long project timelines, and contested credibility with environmental stakeholders means this category is not generating the kind of breakout media attention seen in SMR or green hydrogen. For incumbents, this is currently a relatively stable space, but the underlying narrative tensions – scepticism about CCS as a genuine decarbonisation tool versus its advocacy as an industrial necessity – have not been resolved.

Energy Industry Scan 2026

Download the Onclusive Energy Report to access the full data, understand the energy sector disruptors, the media intelligence methodology, and the complete narrative mapping from the February 28 crisis window.

The full Onclusive Energy Industry Scan (May 2026) delivers the complete dataset: share-of-voice rankings for 10 major players (Shell, ExxonMobil, TotalEnergies, PDVSA, etc.), LinkedIn owned vs. earned media performance, top hashtags, consumer sentiment on fuel prices and outages, CEO visibility, and segment-specific challenges including Trump’s deregulation, AI-driven demand, and retail energy challengers.

Practical signals for competitive intelligence professionals

The Onclusive Energy Industry Scan is not primarily a retrospective document. Its analytical value for competitive intelligence professionals lies in using the patterns it identifies to anticipate where the next narrative disruption will occur. Several practical signals emerge from the data.

Track growth trajectory alongside share of voice. A challenger holding 3% share with a 9/10 growth trajectory is a more significant threat than a challenger holding 15% share with a 5/10 growth trajectory. The former is accelerating; the latter has plateaued. Standard SOV dashboards that report share without trajectory miss the most important competitive intelligence signal.

Monitor the specificity of challenger claims. Stegra’s media position was built on a single, auditable, specific claim. The moment a challenger in your category makes a claim of that kind – a named facility, a signed PPA, a regulatory milestone – the narrative window begins to close for competitors. Detecting that claim in real time, rather than six months later, is the difference between having a response window and not having one.

Watch the hyperscaler adjacency. The most powerful amplifier in the energy narrative landscape in 2026 is the AI electricity demand story. Challengers who have successfully positioned themselves as solutions to the hyperscaler demand problem – SMR developers above all – are receiving a narrative subsidy from one of the highest-attention stories in global business media. Any challenger that achieves a credible connection to this narrative, in any category, will see accelerated coverage growth. Monitor which challengers in your space are beginning to make this connection.

Separate earned from owned in challenger SOV analysis. The most durable competitive positions are built on earned media – third-party coverage generated by what a company does rather than what it says. Challengers who are growing their SOV primarily through owned LinkedIn content and press releases are building a fragile position. Challengers who are generating analyst commentary, consumer advocacy, and investigative journalism are building something much harder to displace. Distinguishing between these two dynamics in a competitor’s media profile is essential intelligence.

Identify the narrative claim that defines the category you are most exposed to. In each of the three categories where new entrants lead, there is a single narrative claim that has become the de facto definition of the space. For green hydrogen: the world’s first large-scale green steel mill. For SMR: reliable low-carbon baseload for AI data centres. For retail energy: technology-driven customer experience that legacy utilities cannot match. The question for incumbents is whether they have a comparable claim in the categories most important to their strategic positioning – and if not, when they intend to make one.

What to do before your window closes

The Energy Industry Scan data suggests a consistent strategic logic across all seven categories analysed: challenger share and growth trajectory move together, and they compound. The window for incumbents to compete for narrative leadership in the categories they did not invent is real, but it is not unlimited.

For communications and competitive intelligence teams, the practical priority is diagnosis. Before developing a response strategy, understand precisely where your organisation sits in the narrative landscape of your most strategically important categories. Are you the established voice, or are you already playing catch-up? Is the challenger in your space building earned credibility or volume alone? Is the growth trajectory in your category moving in one direction or showing signs of plateauing?

The Onclusive Energy Industry Scan provides the analytical infrastructure to answer those questions with data rather than intuition. Share of voice across 86 companies, growth trajectory analysis across seven disruptor categories, earned versus owned media breakdowns, and the topic-level intelligence that reveals where the next narrative shift is forming – these are the inputs that allow communications teams to act before the window closes rather than after.

The full Onclusive Energy Industry Scan (May 2026) delivers the complete dataset: share-of-voice rankings across 86 energy companies, LinkedIn owned vs. earned media performance, CEO visibility analysis, consumer topic analysis, and competitive intelligence across seven disruptor categories. Download the report or arrange a demo to see how Onclusive’s media monitoring and social listening tools can support your competitive intelligence function.

The cover image was generated by a generative AI tool for illustrative purposes.